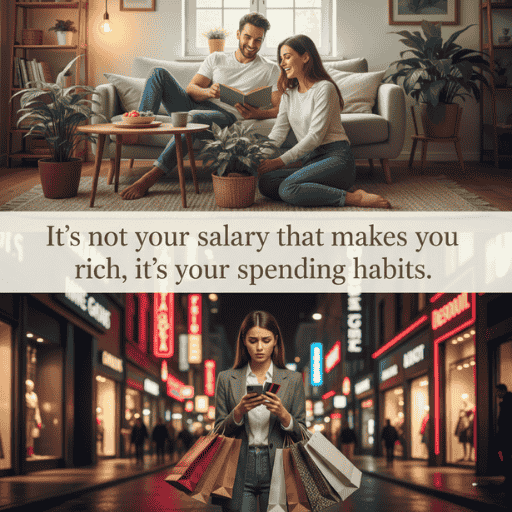

It's not your salary that makes you rich, it's your spending habits.

By: Charles A. Jaffe | Published on Feb 26,2026

Category Spiritual Quotes

About This Quote

This simple yet powerful financial truth comes from Charles A. Jaffe, an American financial journalist and author who has spent decades helping people understand the psychology of money. Jaffe writes about personal finance not as a math problem but as a behavioral challenge—because managing money well isn't about knowing what to do (that's easy), it's about actually doing it (that's hard).

This quote cuts through all the complexity of personal finance to reveal a fundamental truth: wealth is not determined by how much you earn, but by the gap between what you earn and what you spend. You can make six figures and be broke if you spend seven figures. You can make modest income and build real wealth if you consistently spend less than you earn. The equation is simple. The execution is where most people fail.

Why It Resonates

Think about how you approach money. When you get a raise, what happens? You upgrade your lifestyle. New car. Nicer apartment. More expensive restaurants. Better clothes. Suddenly, your increased income is fully absorbed by increased spending. You're making more money but you're not actually wealthier. You're just spending at a higher level.

This is called "lifestyle inflation" or the "hedonic treadmill." Every time your income increases, your spending increases to match. You never actually get ahead. You just spend more while feeling the same level of financial stress.

You look at wealthy people and think: "If I just made what they make, I'd be fine." But that's probably not true. Because your problem isn't your income—it's your spending habits. Give yourself twice your current income, and within six months, you'd probably be spending twice as much. Same stress. Same feeling of never having enough. Just bigger numbers.

Meanwhile, there are people making half what you make who have more savings, less debt, and more financial peace. Not because they're smarter or luckier. Because they have better spending habits. They've developed self-control with money. They can see something they want and choose not to buy it. They can have money available and choose not to spend it.

That ability—self-control with money—is worth more than a raise. It's the difference between building wealth and just earning money.

The Psychology Behind It

Research in behavioral economics reveals that humans are terrible at delayed gratification when it comes to money. The famous "marshmallow test" with children applies to adults too: we struggle to wait for larger future rewards when smaller immediate rewards are available. That impulse purchase, that upgrade, that "treat yourself" moment—those are the marshmallows we can't resist eating.

Studies show that self-control is like a muscle—it can be strengthened or depleted. People who make many decisions throughout the day (decision fatigue) show reduced financial self-control. This is why you're more likely to make impulse purchases when you're tired, stressed, or overwhelmed. Your self-control reserves are depleted.

There's fascinating research on "mental accounting"—how people treat money differently based on arbitrary categories. You might carefully budget grocery spending but freely spend on "entertainment." You might save pennies on gas prices but waste thousands on unused subscriptions. The money is the same, but your self-control varies wildly based on how you've categorized the spending.

Research on the psychology of spending shows that people experience more pleasure from anticipating purchases than from actually having the purchased item. You fantasize about the new phone, the new car, the new clothes. You buy them. Brief spike of pleasure. Then adaptation—you quickly get used to the new thing and it becomes your baseline. The pleasure fades, but the money is gone forever.

Studies on wealth accumulation consistently show that high earners who spend everything are less financially secure than moderate earners who consistently save. The amount you keep matters infinitely more than the amount you earn. This is why lottery winners often end up broke—high income without spending habits to match.

The Deeper Meaning

This quote is really about the distinction between income and wealth. Income is money flowing through your hands. Wealth is money you keep. Most people focus obsessively on increasing income while completely ignoring the leak—their spending habits.

It's like trying to fill a bathtub with the drain open. You can increase the water pressure (earn more), but if the drain is wide open (spending everything you make), the tub never fills. Close the drain (control spending), and even a small stream of water (modest income) will eventually fill the tub.

"It's not your salary that makes you rich"—this challenges the fundamental assumption most people operate under: that the solution to money problems is more money. Get a better job. Get a raise. Win the lottery. But if your spending habits don't change, more money just means more spending. The problem isn't solved—it's just scaled up.

"It's your spending habits"—this is both liberating and terrifying. Liberating because it means you have control. You don't need a raise to improve your financial situation—you need better habits. Terrifying because it means you can't blame external circumstances. Your financial struggles are mostly self-inflicted through lack of spending discipline.

The deeper wisdom is about self-control as the foundation of financial success. You can learn all the investment strategies, optimize your tax situation, maximize your income—but if you can't control your spending, none of that matters. Self-control with money is the prerequisite for every other financial goal.

And self-control isn't about deprivation—it's about knowing the difference between what you want in the moment and what you want most. In the moment, you want the new gadget. But what you want most is financial security, freedom from debt, the ability to retire someday. Self-control is choosing what you want most over what you want now.

Living This Truth

Track every dollar you spend for one month. Not to judge yourself, just to see the truth. You cannot control what you don't measure. Most people are shocked when they actually see where their money goes. Awareness is the first step to control.

Implement the 24-hour rule for non-essential purchases. See something you want to buy? Wait 24 hours. If you still want it tomorrow, consider it. Most impulse purchases lose their appeal when you introduce any delay between desire and action.

Separate wants from needs ruthlessly. You need food, shelter, basic clothing, transportation to work. Almost everything else is a want pretending to be a need. Your mind will tell you that you "need" the upgrade, the convenience, the premium version. Question that. Do you need it, or do you want it?

Automate saving before you can spend. The money you never see is the money you don't spend. Set up automatic transfers to savings the day your paycheck arrives. Pay yourself first. What's left over is what you have permission to spend.

Calculate purchases in hours of work, not dollars. That $200 purchase? That's X hours of your actual life, converted to money, then converted to this thing. Is this thing worth X hours of your finite life? This reframe changes the equation.

Practice saying no to yourself. Not because you can't afford it, but because you're choosing not to spend it. This is the muscle of self-control. Every time you see something you could buy but choose not to, you're strengthening that muscle.

And audit your recurring expenses mercilessly. Subscriptions, memberships, services—these bleed money continuously because they're invisible. Cancel anything you're not actively using. Even small recurring expenses add up to massive amounts over time.

Your Reflection Today

If your income doubled tomorrow, what would happen to your spending? Be honest—would you save the extra, or would your lifestyle inflate to match?

What purchases have you made in the past month that you could have gone without? Not "shouldn't have made," but genuinely could have been fine without?

What's one spending habit you could change this week that would meaningfully improve your financial situation?

Here's what Charles Jaffe wants you to understand: You're probably not broke because you don't earn enough. You're broke because you spend everything you earn. And often more.

You look at your income and think "if I just made more, I'd be fine." But that's a lie you're telling yourself. Because when you made less than you do now, you said the same thing. And when you make more than you do now, you'll say it again. The problem isn't the amount—it's the habit.

Your spending rises to meet your income. Always. Unless you deliberately develop the self-control to prevent it.

This is why people making $200,000 a year feel just as broke as people making $50,000. Different numbers, same problem. They spend everything they make. No matter what they make, they spend it all. And then they wonder why they're not wealthy.

Meanwhile, there are people making modest incomes who are building real wealth. Not because they have secret investment strategies or financial genius. Because they have one simple habit: they consistently spend less than they earn. They save the difference. They invest it. Over time, that gap between income and spending compounds into actual wealth.

That's the only path to wealth that actually works: spend less than you earn, consistently, over time. Everything else is details.

But that requires self-control. The ability to see something you want and choose not to buy it. The ability to have money and choose not to spend it. The ability to resist the constant cultural pressure to upgrade, to keep up, to treat yourself.

Most people don't have that self-control. They see money as something to spend. They see their bank balance as permission to buy. They see sales as savings (when they're actually spending). They see wants as needs. They see "affordable monthly payments" without calculating the total cost.

And then they wonder why they're not rich.

It's not your salary that makes you rich. You could make a fortune and still be broke if you spend a fortune plus one dollar. You could make a modest income and build real wealth if you consistently spend a modest income minus one dollar.

The math is simple. The psychology is hard.

Because spending feels good in the moment. Saving feels like deprivation. Buying something gives you immediate pleasure. Not buying something gives you... nothing. At least nothing immediate. The benefit of not spending only shows up later, in the form of savings, investments, financial security. But your brain wants pleasure now, not security later.

So you spend. You rationalize. You tell yourself you deserve it, you work hard, life is short, you'll save more later. And "later" never comes because later, you'll have the same spending habits you have now.

Unless you change them. Unless you develop self-control with money. Unless you learn to distinguish wants from needs. Unless you practice saying no to yourself. Unless you make spending decisions based on what you want most (financial freedom) instead of what you want now (the thing in front of you).

Your salary doesn't make you rich. Your spending habits do.

So change your habits. Track your spending. Question your purchases. Delay gratification. Automate saving. Calculate costs in hours of life.

And most importantly: stop waiting for more income to fix your money problems. Fix your spending habits instead.

That's where wealth comes from. Not from earning more. From keeping more.

Control your spending. Build your wealth. 💰✨

.png)

.png)

Amazon Affiliate Disclosure

As an Amazon Associate I earn from qualifying purchases.

Comments

No comment yet. Be the first to comment